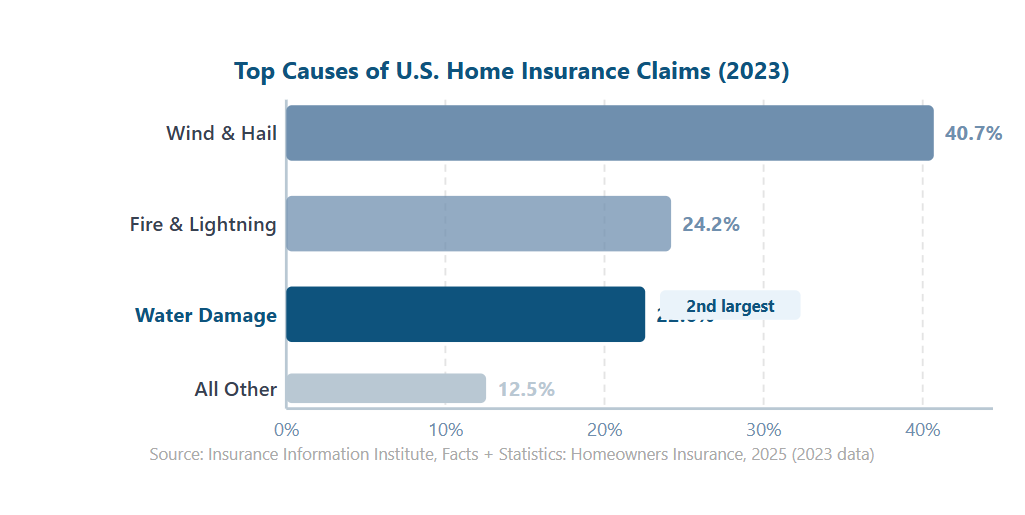

In the U.S., 1 in 67 insured homes files a water damage or freezing claim every year — the second-largest category of home insurance losses, accounting for 22.6% of all claims, according to the Insurance Information Institute’s 2025 Facts + Statistics report on homeowners insurance. Most Texas homeowners don’t know how to file a water damage insurance claim in Texas — or that they’re already in that 1-in-67 window — until water is already on the floor.

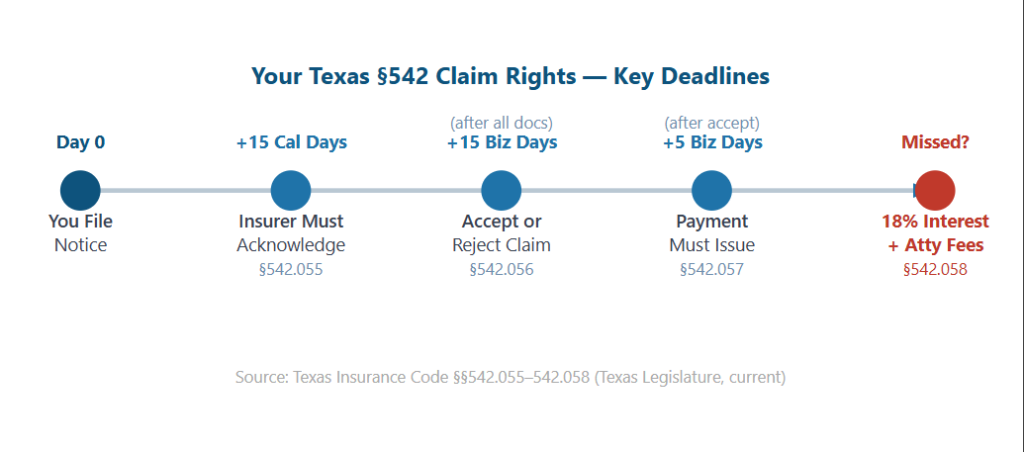

What they also don’t know: Texas has some of the most homeowner-favorable insurance payment laws in the country. Texas Insurance Code §542 gives insurers hard deadlines — and gives you an 18% annual interest penalty plus attorney’s fees when they miss them. Most guides never mention it. This one leads with it.

This guide walks through every step from the first 60 minutes to final payment — including our water damage restoration process and the Texas-specific legal rights most adjusters hope you don’t know.

Key Takeaways

- In 2023, water damage and freezing accounted for 22.6% of all U.S. homeowners insurance losses — the second-largest claim category (Insurance Information Institute, 2025).

- Texas Insurance Code §542 requires insurers to acknowledge your claim within 15 calendar days and approve or deny within 15 business days of receiving all required documentation.

- Most Texas water damage claim denials involve gradual damage, exterior flooding without flood coverage, or failure to mitigate — all preventable with immediate professional response.

- Mold can begin growing within 24–48 hours of water exposure (Texas Department of Insurance). A delay that produces mold converts a single water damage claim into a contested, sub-limited mold claim.

Does Texas Homeowners Insurance Cover Water Damage?

Standard Texas homeowners insurance covers sudden and accidental water damage from internal sources — but mold remediation is capped at $5,000–$25,000 on most HO-A and HO-B policies under Texas Department of Insurance Commissioner Order CO-01-1105, and flooding from outside your home is excluded entirely. Knowing which side of that line your damage falls on determines whether your claim gets paid.

What standard Texas homeowners insurance typically covers:

- Burst pipes (sudden and accidental)

- Ice maker and refrigerator supply line failures

- Water heater ruptures

- Dishwasher and washing machine overflows

- HVAC condensate drain overflows

- Roof intrusion caused by a covered peril (hail or wind damage — both common in DFW)

What it typically does NOT cover:

- Flooding from outside — rising water, storm surge, overland flow (requires a separate NFIP or private flood policy)

- Gradual damage — a slow drip, seeping foundation, or pinhole leak the homeowner “knew or should have known about”

- Sewer and drain backup (unless you purchased a sewer backup endorsement)

- Mold remediation above the policy sub-limit ($5,000–$25,000 on most Texas HO-A/HO-B policies)

The line between “sudden” and “gradual” is where most Texas water damage claims get disputed. An adjuster who arrives three days after a slow leak began may argue the damage is gradual. A licensed restoration contractor who documents sudden onset with date-stamped moisture readings on Day 1 tells a different story.

Water damage is one of the leading causes of home insurance claims, making fast cleanup and professional restoration important after leaks, floods, or plumbing failures. SS Water Restoration serves homeowners and businesses throughout the Dallas-Fort Worth area.

SVG file: assets/chart-01-home-insurance-claim-causes.svg

Caption: Water damage and freezing is the second-largest cause of U.S. homeowners insurance claims. In Texas, with 8.1 million active policies, that means hundreds of thousands of claims filed each year. Source: Insurance Information Institute, 2025.

In 2023, water damage and freezing accounted for 22.6% of all U.S. homeowners insurance losses — the second-largest claim category — according to the Insurance Information Institute’s 2025 Facts + Statistics report on homeowners insurance. Standard Texas HO-A and HO-B policies cover sudden internal water damage but cap mold remediation at $5,000–$25,000 under Texas Department of Insurance Commissioner Order CO-01-1105 (effective 2002–2003, still in force).

To understand what restoration will cost if a claim is approved, see water damage restoration costs in DFW.

What Should You Do in the First 60 Minutes After Water Damage?

Water on hardwood flooring can quickly lead to swelling, cupping, staining, and hidden moisture damage. SS Water Restoration provides emergency water extraction, drying, and floor damage restoration services across Dallas and Fort Worth.

The Texas Department of Insurance confirms mold can begin within 24–48 hours of water exposure, and every hour of active water contact expands the moisture footprint behind walls and under floors. Every minute of active water contact increases restoration scope — and those first 60 minutes are your window to document sudden onset — the evidence that separates a covered sudden-and-accidental claim from an excluded gradual-damage denial. Here’s what to do immediately, in order.

- Stop the source. Shut off the water main or the isolation valve closest to the failure. For an HVAC condensate overflow, turn off the system. Don’t let water keep flowing while you figure out what to do next.

- Check safety first. If water is near an electrical panel, breaker box, or outlets, don’t enter the area until you’ve shut off power. Standing water and live electricity is a life-safety issue before it’s an insurance issue.

- Don’t remove or discard anything yet. Every damaged material — carpet, drywall, flooring, cabinetry — is part of your claim scope. Removing it before documentation removes it from your potential payout.

- Start a video walkthrough immediately. Before touching anything, record a narrated video showing all affected areas, water on surfaces, the location of the failure, and any visible damage. Say the date and time on camera. This is evidence. It’s also the fastest thing you can do to establish a timeline.

- Call for professional restoration and notify your insurer. Call a licensed restoration contractor first — they’ll create the professional documentation your adjuster needs while satisfying your policy’s mitigation duty. Then call your insurer to file notice. Both calls should happen within the first hour.

From the field — Stephan Sannikov, IICRC Certified, License #RCO1659:

“In almost every disputed Texas claim we see, the problem started in the first hour. A homeowner tried to clean it up themselves, moved materials before documenting them, or waited 48 hours because it looked minor. By the time we arrived, the moisture had migrated behind walls, the adjuster had already walked the property, and the documentation that could have proven sudden onset was gone. The video walkthrough you do in the first 15 minutes is worth more than anything we can reconstruct after the fact.”

How to Document Water Damage for Your Insurance Claim

In 2024, Texas had 8.1 million active homeowners insurance policies (Texas Department of Insurance, 2024) — and under §542.056, every one of those policyholders faces the same rule: the 15-business-day decision clock doesn’t start until complete documentation has been received. Professional documentation doesn’t just support your claim — it starts the Texas Insurance Code §542.056 clock. Under §542.056, your insurer’s 15-business-day window to accept or reject your claim doesn’t begin until they’ve received “all required documentation.” A complete packet from a licensed restoration contractor is what triggers that deadline.

Here’s the exact documentation SS Water Restoration submits at every DFW job — the packet we send to Travelers, USAA, State Farm, Safeco, Nationwide, Allstate, and American Family:

- Date-stamped moisture readings at intake — Recorded at every affected surface before any equipment is placed. This is the “sudden onset” baseline. Dry readings on Day 1 don’t exist in a gradual-leak scenario.

- Equipment placement log — Serial numbers, locations, and deployment timestamps for all dehumidifiers, air movers, and desiccant equipment. Proves mitigation began immediately.

- Daily drying logs — Moisture readings at each monitoring visit, showing progress toward IICRC S500 dry standard targets.

- Line-item scope of work — Every affected material, required treatment, and restoration steps.

- Time-stamped photo records — All affected areas, equipment placement, and material condition at each visit.

- Certificate of completion — Final moisture readings confirming all materials reached dry standard.

All seven insurers above accept this as complete documentation for §542.056 purposes. When we submit it, your adjuster’s 15-business-day decision clock starts.

What you should document yourself (before we arrive):

- Narrated video walkthrough with date and time stated on camera

- Still photos of the failure source and all affected rooms

- Written inventory of damaged property with estimated replacement costs

- Receipts for any emergency supplies purchased (tarps, wet-dry vac, towels)

The more first-hour documentation exists, the harder it is for an insurer to reclassify sudden damage as gradual.

How to File the Claim: From First Call to Final Payment

Under Texas Insurance Code §542, your insurer must acknowledge your claim within 15 calendar days of notice, accept or reject it within 15 business days of receiving complete documentation, and issue payment within 5 business days of acceptance. Late payments trigger 18% annual interest plus attorney’s fees under §542.058. That statutory framework sits behind every step below.

Step 1: Notify your insurer. Call your insurance company’s claims line as soon as the source is stopped and safety is confirmed. Give basic facts only: policy number, date and time discovered, and known cause. Don’t speculate about coverage, total damage, or whether you think it’s covered.

Step 2: File written notice. Follow your phone call with a brief email or certified letter. “I am providing written notice of a water damage loss at [address] that occurred on [date].” This creates a documented timestamp — Day 0 on the §542.055 acknowledgment clock.

Step 3: Submit your complete documentation packet. Compile the restoration contractor’s documentation with your personal records (video, photos, inventory). Submit as a single organized package. This triggers the 15-business-day §542.056 decision deadline.

Step 4: Prepare for the adjuster visit. The insurer will send an adjuster. Walk them through every affected area. Have your documentation available. Don’t minimize or exaggerate — just show what’s there and let the numbers speak.

Step 5: Review the Scope of Loss before signing. The adjuster produces a Scope of Loss listing what they’ll pay for. Compare it against the restoration contractor’s scope. Watch for: missing line items, incorrectly applied depreciation, or reconstruction scope the insurer wants to exclude.

Step 6: Understand ACV vs. RCV. Actual Cash Value policies pay what damaged materials were worth at time of loss (depreciated). Replacement Cost Value policies pay what it costs to replace them. Know which type you have before you sign anything.

Step 7: Complete the Proof of Loss. Texas policies typically require a sworn Proof of Loss within 91 days of the loss event. Missing this deadline can void your claim regardless of coverage. Your restoration contractor can help compile the numbers.

Texas insurance claim deadlines can move quickly after water damage. SS Water Restoration helps Dallas-Fort Worth homeowners and businesses document damage, mitigation, drying, and restoration work during the claims process.

Caption: Texas §542 gives homeowners hard deadlines backed by an 18% annual interest penalty plus attorney’s fees for late payment. Most Texas homeowners don’t know these rights exist. Source: Texas Insurance Code §§542.055–542.058.

Texas Insurance Code §542.055 requires insurers to acknowledge a claim within 15 calendar days. Under §542.056, they must accept or reject within 15 business days of receiving all required documentation. §542.057 mandates payment within 5 business days of acceptance. Under §542.058, late payments incur 18% annual interest plus attorney’s fees — one of the strongest homeowner protections available in any U.S. state (Texas Legislature, current).

For context on how long the restoration work runs alongside this claims process, see our guide on how long water damage restoration takes in DFW.

Your Texas Legal Rights Under Insurance Code §542

Texas Insurance Code §542.058 imposes an 18% annual interest penalty on late insurance payments, plus reasonable attorney’s fees — and knowing violations can trigger treble damages. Most Texas homeowners have never heard of this. But insurers know it exists. A properly filed demand letter at Day 16 of non-acknowledgment costs an insurer more than most residential water damage claims are worth. That’s leverage.

Most guides frame §542 as a timeline to understand. It’s actually a tool to use.

Floodwater around a home can quickly enter garages, crawl spaces, walls, and flooring. SS Water Restoration provides emergency flood cleanup, water extraction, drying, and restoration services throughout Dallas and Fort Worth.

If your claim stalls, here’s how to use §542 step by step:

At Day 16 after filing notice: If you haven’t received written acknowledgment, send a certified letter to your insurer citing Texas Insurance Code §542.055, the date you filed notice, the deadline that has passed, and your claim details. Keep it factual. Demand written acknowledgment within 5 business days. This letter alone often breaks a stalled claim loose.

After the 15-business-day decision deadline: If your insurer received your complete documentation and hasn’t responded, send a second certified demand letter citing §542.056 with the submission date of your documentation and the deadline date that passed.

File a TDI complaint. The Texas Department of Insurance handles consumer insurance complaints at tdi.texas.gov/consumer/complain.html. Insurers must respond to TDI complaints within 45 days. This goes on the insurer’s regulatory record and often produces a resolution faster than any follow-up call.

When to consider a public adjuster. For claims over $20,000, disputed scope, or denied claims with apparent coverage, a licensed Texas public adjuster represents your interests — not the insurer’s. They’re paid a percentage of the final settlement.

When to consider an insurance attorney. If TDI complaints produce nothing, if the insurer is acting in bad faith, or if total claim value justifies legal fees, an attorney can pursue treble damages under §542.058’s knowing-violation clause.

Texas Insurance Code §542.058 imposes 18% annual interest on late insurance payments plus reasonable attorney’s fees. Knowing or intentional violations may result in treble damages. This makes late payment more expensive than most residential water damage claims — giving homeowners who know how to invoke it significant legal leverage when insurers delay or underpay (Texas Insurance Code §542.058, current; Haun Mena Law analysis, 2025).

Does Flood Damage Fall Under Your Texas Homeowners Policy — or Require Separate NFIP Coverage?

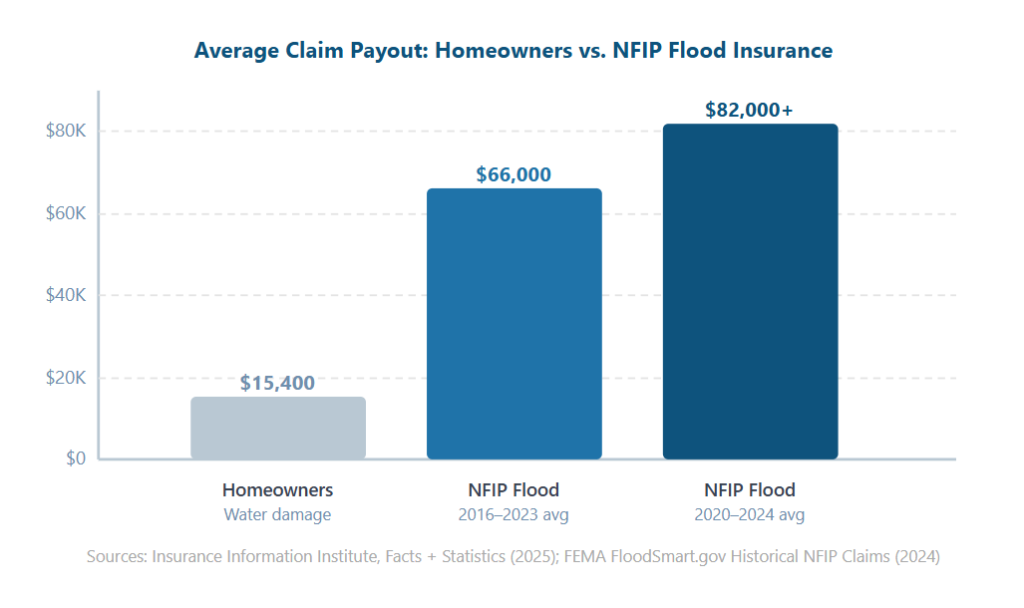

Standard Texas homeowners insurance does not cover flooding from outside your home. The numbers make the gap impossible to miss: according to the Insurance Information Institute’s 2025 Facts + Statistics report (2019–2023 data), the national average homeowners water damage claim paid $15,400. According to FEMA’s FloodSmart.gov historical NFIP claims data, the average NFIP flood insurance claim paid $66,000 for the 2016–2023 period and exceeded $82,000 for 2020–2024. That’s not a minor difference. It reflects the fact that these are two entirely separate products covering two entirely different events.

Floodwater can enter homes through doors, garages, and foundation openings even when sandbags are used. SS Water Restoration provides emergency water removal, drying, and flood damage restoration across Dallas and Fort Worth.

The coverage divide in plain English:

- Interior water damage — a burst pipe, appliance overflow, HVAC failure, or roof intrusion from a covered peril → your standard homeowners policy

- Exterior flooding — rising water from rain, creek overflow, storm surge, overland flow → requires NFIP or private flood insurance

NFIP basics:

The National Flood Insurance Program offers up to $250,000 in building coverage and $100,000 in contents coverage for residential properties. Critical detail: there’s a 30-day waiting period before coverage takes effect. You can’t buy flood insurance 48 hours before a storm. It has to already be in place.

Texas NFIP context:

In 2023, Texas had 586,680 NFIP policies in force at a median cost of $779 per year, according to FEMA’s FloodSmart.gov data. The Texas NFIP program has paid 160,985 claims totaling $7.48 billion since inception. Hurricane Harvey alone averaged $146,589 per NFIP claim (Insurance Information Institute).

DFW-specific considerations:

Dallas–Fort Worth isn’t a coastal flood zone, but heavy rain events and creek/drainage system backups do occur — especially in creek-adjacent neighborhoods like Las Colinas, Lewisville, and parts of Plano. More relevant to most DFW homeowners: sewer backup coverage. Sewer backup is excluded from both standard homeowners policies and NFIP. It requires a separate endorsement — typically $50–$100/year — and it’s worth adding. Flood-related claims can result in much higher average payouts than standard homeowners water damage claims. SS Water Restoration helps Dallas-Fort Worth property owners respond quickly with water extraction, drying, documentation, and restoration services.

Caption: The NFIP flood insurance average payout is 4–5× higher than the standard homeowners water damage average — because they cover events of completely different scale. Standard homeowners covers interior pipe failures. NFIP covers the kind of flooding that Hurricane Harvey produced. Sources: Insurance Information Institute, 2025; FEMA FloodSmart.gov, 2024.

The national average homeowners insurance water damage claim paid $15,400 (2019–2023 data), while the NFIP flood insurance average was $66,000 for 2016–2023 and exceeded $82,000 for 2020–2024, according to the Insurance Information Institute’s 2025 Facts + Statistics report and FEMA’s FloodSmart.gov historical claims data. The difference is not a matter of coverage quality — it reflects entirely different events covered by entirely different policies.

Why Water Damage Claims Get Denied in Texas — and How to Fight Back

The most common reason Texas water damage claims are denied is the gradual damage exclusion — damage that occurred over time from a slow leak, corrosion, or deterioration the homeowner “knew or should have known about,” according to Texas Department of Insurance guidance on water and mold coverage. Gradual damage isn’t covered. Sudden and accidental damage is. The adjuster’s job, in a disputed claim, is to move your damage from the “sudden” column into the “gradual” column.

A leaking or running faucet can quickly lead to standing water, moisture damage, and mold concerns. SS Water Restoration provides emergency water extraction, drying, and cleanup services across Dallas and Fort Worth.

Here are the most common denial reasons in Texas and what you can do about each:

| Denial Reason | Why It Applies | How to Prevent or Counter It |

| Gradual damage / maintenance neglect | Policy excludes deterioration the homeowner should have caught | Document sudden onset; Day 1 date-stamped moisture readings are direct evidence |

| Flooding from outside without flood coverage | Standard HO policies exclude overland flow | Purchase NFIP or private flood policy before any event |

| Sewer or drain backup without endorsement | Backup is a separate policy add-on | Check your declarations page; add endorsement now |

| Mold above sub-limit | Most TX HO-A/HO-B caps mold at $5K–$25K | Purchase mold endorsement; mitigate within 24–48 hrs |

| Failure to mitigate further damage | Policies require reasonable steps to prevent additional loss | Call licensed restoration immediately — they document mitigation from Hour 1 |

| ACV vs. RCV disputes | Depreciation reduces payment below full replacement | Know your policy type; file supplemental claim after repairs complete |

How to fight a denial:

Request the written denial with the specific policy language cited. Then compare that language to the actual definition of “sudden and accidental” in your policy — most Texas HO-A/HO-B policies define this as an unexpected event from a specific, identifiable cause. Date-stamped professional moisture readings from Day 1 are exactly that: a specific, identifiable, timestamped event.

If the denial stands: invoke the appraisal clause (available in most Texas policies) to dispute scope and value independently of coverage questions. File a TDI complaint at tdi.texas.gov/consumer/complain.html. Consult an insurance attorney for suspected bad-faith handling.

Most homeowners fight denials at the wrong stage — in appeals, weeks after the fact. The real fight happens on Day 1 when moisture readings are recorded, the failure source is documented, and the timeline of events is locked in writing by a licensed contractor. An adjuster can’t reclassify damage as gradual when you have date-stamped professional readings showing dry conditions 24 hours earlier. That’s not a legal argument. It’s evidence. And evidence wins claims.

For sewage backup restoration specifically, Category 3 contamination applies from Hour 1 — the gradual damage question doesn’t arise, but documentation of contamination scope at intake is equally important for claim purposes.

How Does the 24–48 Hour Mold Window Affect Your Texas Insurance Claim?

Mold can begin growing within 24–48 hours of water exposure, according to the Texas Department of Insurance’s guidance on water and mold coverage. Most Texas HO-A and HO-B policies cap mold remediation at $5,000–$25,000 under TDI Commissioner Order CO-01-1105. Once visible mold establishes itself — and once your claim crosses from “water damage” into “mold remediation” — those two facts collide in a way that can leave a significant out-of-pocket gap.

This isn’t an edge case. In Dallas–Fort Worth summers, with June relative humidity averaging 67% according to NOAA NWS Fort Worth’s 1991–2020 climate normals, wet structural materials stay moist longer than in drier climates. The biological clock runs faster here than most national guidelines assume.

From the field — Stephan Sannikov, IICRC Certified, License #RCO1659:

“We were called to a Plano townhome last August — Category 1 water from an HVAC condensate overflow on the second floor. The homeowner had tried to manage it themselves for two days with towels and a box fan. By Day 3, we found mold colonies on the drywall behind the baseboard. The insurer’s position: delayed mitigation converted the water damage claim into a mold claim subject to the $10,000 sub-limit. Our intake equipment logs showed we weren’t there on Day 1 — because we hadn’t been called. The homeowner’s out-of-pocket gap was $8,200. If we’d arrived that first day, applied antimicrobial treatment, and documented clean surfaces at intake, that claim stays in the water damage category. Timing mattered more than anything else in that job.”

What the mold timeline means for your claim:

- Mold remediation on typical residential scope runs $1,200–$3,750 for containment and treatment (Angi, 2026 cost guide) — within most sub-limits for a contained area. But mold in wall cavities, subfloor systems, or HVAC ducts can exceed $25,000.

- Insurers may argue that mold resulted from your failure to mitigate rather than from the original water event — particularly if 48+ hours passed without professional response.

- SS Water Restoration applies EPA-registered antimicrobial treatment at every job on Day 1. This creates a documented record that surfaces were treated before mold could establish — protecting your claim from the mitigation-failure argument.

For jobs where mold is already confirmed at intake, see our mold remediation services in DFW.

SS Water Restoration responds within 60 minutes anywhere in DFW — 24 hours a day, 7 days a week. We handle direct insurance billing with Travelers, USAA, State Farm, Safeco, Nationwide, Allstate, and American Family. From the first hour, we provide the complete documentation package your adjuster needs to start the Texas §542 clock: date-stamped moisture readings, equipment logs, daily drying records, scope of work, and time-stamped photo records.

Call [(469) 737-0296](tel:4697370296) now.

Frequently Asked Questions

Does homeowners insurance cover water damage in Texas?

Standard Texas homeowners insurance covers sudden and accidental water damage from internal sources — including burst pipes, appliance overflows, water heater failures, and HVAC condensate drain backups. In 2023, water damage and freezing accounted for 22.6% of all U.S. homeowners insurance losses, making it the second-largest claim category, according to the Insurance Information Institute’s 2025 Facts + Statistics report on homeowners insurance. However, standard Texas HO-A and HO-B policies do not cover flooding from outside the home, gradual damage from a slow leak or corrosion, or sewer and drain backup without a specific endorsement. Mold remediation coverage is capped at $5,000–$25,000 on most Texas policies under Texas Department of Insurance Commissioner Order CO-01-1105. If you have any doubt about whether your specific damage is covered, call your insurer and request written confirmation before agreeing to any scope of repairs. The Texas Department of Insurance maintains a free consumer helpline at 1-800-252-3439 for coverage questions.

How long does an insurance company have to settle a water damage claim in Texas?

Under Texas Insurance Code §542 — the state’s prompt-payment statute — your insurer must follow a specific deadline sequence after you file a water damage claim. Under §542.055, the insurer must acknowledge receipt of your claim and begin investigation within 15 calendar days of notice. Under §542.056, once you’ve submitted all required documentation, the insurer has 15 business days to accept or reject your claim; this window can be extended by 45 days with written notice explaining the delay. Under §542.057, once your claim is accepted, payment must be issued within 5 business days. If the insurer misses any of these deadlines, §542.058 triggers: the insurer owes 18% annual interest on the overdue amount plus reasonable attorney’s fees. Knowing or intentional violations may result in treble damages. If your insurer isn’t meeting these deadlines, send a certified demand letter citing the specific statute section and the date the deadline passed. Follow with a complaint to the Texas Department of Insurance at tdi.texas.gov/consumer/complain.html.

What documentation do I need for a water damage insurance claim in Texas?

Documentation for a Texas water damage insurance claim falls into two categories: what you provide and what a licensed restoration contractor provides. For your documentation: a narrated video walkthrough of all affected areas recorded immediately after the event (with date and time stated on camera), still photos of the failure source and all affected rooms, a written inventory of damaged property with estimated replacement costs, and receipts for any emergency mitigation supplies. For contractor documentation — which is what actually starts the Texas §542.056 claim decision clock — SS Water Restoration provides at every DFW job: date-stamped moisture readings at intake establishing sudden onset, equipment placement logs proving mitigation began immediately, daily drying logs showing progress toward IICRC S500 dry standard, a line-item scope of work, time-stamped photo records, and a certificate of completion. This complete packet is accepted by Travelers, USAA, State Farm, Safeco, Nationwide, Allstate, and American Family. The §542.056 clock starts the day your insurer receives it.

Why do water damage insurance claims get denied in Texas?

The most common reason Texas water damage claims are denied is the gradual damage exclusion — damage that occurred over time from a slow leak or corrosion the homeowner “knew or should have known about,” according to Texas Department of Insurance guidance on water and mold coverage. Other common denial reasons include: flooding from outside the home without a separate NFIP or private flood policy; sewer backup without a specific endorsement; and mold costs that exceed the $5,000–$25,000 sub-limit most Texas HO-A/HO-B policies carry under TDI Commissioner Order CO-01-1105. Insurers may also reduce or deny claims citing “failure to mitigate” — arguing that delayed action allowed damage to worsen beyond what the original event caused. The best defense against all of these denials is immediate professional response: a licensed restoration contractor arriving on Day 1 documents sudden onset with date-stamped moisture readings, applies antimicrobial treatment, and creates a paper trail that makes the gradual damage argument very difficult to sustain.

Does flood insurance pay more than homeowners insurance for water damage?

Yes — significantly more, because they cover different events at different scales. Standard Texas homeowners insurance covers interior water damage from pipes and appliances, with a national average claim payout of $15,400, according to the Insurance Information Institute’s 2025 Facts + Statistics report (2019–2023 data). Note: the III dataset explicitly excludes Texas from its homeowners claim averages. The National Flood Insurance Program covers flooding from exterior sources — rising water, storm surge, overland flow — and paid an average of $66,000 per claim for 2016–2023 and more than $82,000 per claim for 2020–2024, according to FEMA’s FloodSmart.gov historical claims data. Hurricane Harvey alone averaged $146,589 per NFIP claim (Insurance Information Institute). In Texas, 586,680 NFIP policies were active as of 2023 at a median annual cost of $779. The 30-day waiting period means flood insurance must be purchased before a storm event — not during one. DFW homeowners should treat standard homeowners coverage and NFIP flood coverage as two separate tools for two separate risks.

Conclusion

Filing a water damage insurance claim in Texas is more manageable when you know the rules. Document everything in the first hour. Call a licensed restoration company before you touch anything — their professional records are what starts the Texas §542 clock and what makes the gradual damage argument hard to sustain. Know the statutory deadlines: 15 calendar days for acknowledgment, 15 business days after complete documentation for a decision, 5 business days after acceptance for payment. Don’t confuse water damage with flood damage — they’re covered by different policies at vastly different payout levels.

SS Water Restoration handles direct billing with seven major Texas insurers and delivers the complete documentation package your adjuster needs from Hour 1. We respond within 60 minutes anywhere in DFW, around the clock.

- Understand what restoration will cost: water damage restoration costs in DFW

- See how long the process takes alongside your claim: water damage restoration timeline for DFW

Sources

1. Insurance Information Institute, “Facts + Statistics: Homeowners and Renters Insurance,” retrieved 2026-05-21, https://www.iii.org/fact-statistic/facts-statistics-homeowners-and-renters-insurance

2. Texas Department of Insurance, “When are water damage and mold covered by insurance?” retrieved 2026-05-21, https://www.tdi.texas.gov/tips/when-are-water-damage-and-mold-covered-by-insurance.html

3. Texas Department of Insurance, Commissioner Order CO-01-1105, “Mold Endorsements,” retrieved 2026-05-21, https://www.tdi.texas.gov/orders/co-01-1105.html

4. Texas Insurance Code Chapter 542, “Processing and Settlement of Claims,” Texas Legislature, retrieved 2026-05-21, https://statutes.capitol.texas.gov/GetStatute.aspx?Code=IN&Value=542

5. Texas Insurance Code §542.056, Justia Law, retrieved 2026-05-21, https://law.justia.com/codes/texas/insurance-code/title-5/subtitle-c/chapter-542/subchapter-b/section-542-056/

6. Texas Insurance Code §542.055, FindLaw, retrieved 2026-05-21, https://codes.findlaw.com/tx/insurance-code/ins-sect-542-055/

7. Haun Mena Law Firm, “Texas Insurance Code Chapter 542 — Understanding Your Rights,” retrieved 2026-05-21, https://haunmena.com/texas-insurance-code-chapter-542/

8. FEMA / FloodSmart.gov, “Historical NFIP Claims Information and Trends,” retrieved 2026-05-21, https://www.floodsmart.gov/historical-nfip-claims-information-and-trends

9. Texas Department of Insurance, “Insurance claim tips for Texans with flooding,” May 2024, https://www.tdi.texas.gov/news/2024/tdi05072024.html

10. Texas Department of Insurance, “Texas Homeowners Insurance Market Overview,” 2024, https://www.tdi.texas.gov/general/texas-homeowners-insurance-market-overview.html

11. Insurify, “Water Damage Statistics: Exploring Costs and Insurance Claims,” retrieved 2026-05-21, https://insurify.com/homeowners-insurance/insights/water-damage-statistics/

12. Angi, “How Much Does Mold Remediation Cost?” 2026, https://www.angi.com/articles/how-much-does-mold-remediation-service-cost.htm

13. NOAA NWS Fort Worth, “DFW Climate Records and Normals,” 1991–2020 30-Year Climate Normals, https://www.weather.gov/fwd/dfwrecordsnormals